Life Insurance and health insurance: Understanding the differences

Life's full of surprises, mate – some good, some not so much. That's why understanding your insurance options is crucial. Considering your options? Well, you might have stumbled upon health insurance and life insurance. Today, we're breaking down both types of cover, highlighting their differences, and exploring how they can complement each other.

The Big Four: Understanding the 4 main types of insurance

1. Life insurance (death cover)

Death cover provides financial support to your family or dependents if you pass away or get diagnosed with a terminal illness. It helps them pay off debts, cover funeral costs, and make up for lost income.

Here's what's on the table:

Death benefit: A lump sum payment for your loved ones if you happen to pass away, leaving them a financial safety net.

Child’s critical illness benefit: Got little ones? This got your back with cover for them too. Think of it as a little cushion for unexpected bumps along the way.

Terminal illness benefit: If you're given less than 12 months to live, insurers offer an early payout to help you and your family through the tough times.

Future insurability benefit: Life changes, and this benefit allows you to boost your cover without the hassle of additional paperwork if you experience a major life event, including getting married, having a child or taking out a mortgage.

2. Income protection

This insurance protects one of your biggest assets – your income. Just like having a backup battery for your phone, income protection insurance keeps you powered up when you can't work due to illness or injury. It's like having a steady income stream even when you're not punching in at the office.

This means you and your family can cover essential expenses without worrying about financial strain. The payment amount and duration of cover will vary based on your individual circumstances, providing tailored support when you need it most.

3. Critical illness

Also known as Trauma Insurance, this cover gives you a lump sum payment if you're hit with a critical illness or injury, so you can focus on getting back on your feet without worrying about the bills.

Read more about critical illness cover’s key feature and benefits here.

4. Total and Permanent Disability (TPD)

If you're totally and permanently disabled due to illness or injury, this cover gives you a lump sum payment to help cover medical expenses and rehabilitation treatments.

Now, how much will all this cost? Well, that depends on your age, job, lifestyle, and medical history.

Read more about critical illness cover’s key feature and benefits here.

What is health insurance?

This is your personal backup plan for medical stuff. With the right health insurance, you can tackle all sorts of medical bills, from emergency situations to your regular checkups. Think private hospital stays, ambulance rides, intensive care, and even things like dental or physio appointments. Plus, if you've got a specific health condition, your insurance might help with those treatments too.

Now, you're probably already familiar with Medicare and benefiting from it if you're living in Australia. It takes care of a lot of your medical bills already. But having private health insurance gives you some extra perks. You get more options for healthcare and, sometimes, faster treatment since you're a private patient.

Having health insurance could even save you some cash come tax time. Yep, you might be eligible for the private health insurance tax rebate. Check out the deets with the ATO for all the nitty-gritty.

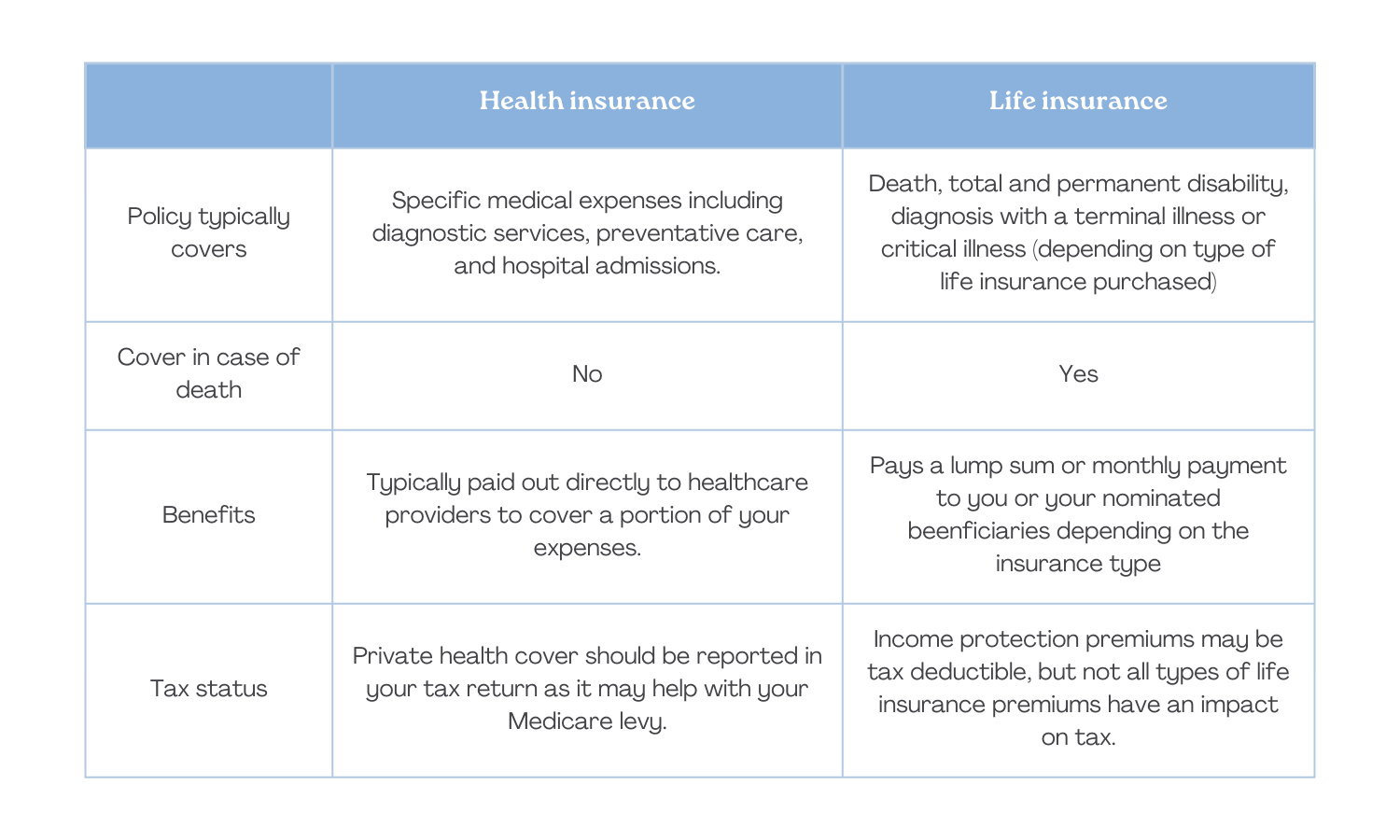

Life insurance vs. health insurance

So, what sets life insurance apart from health insurance? While they're different beasts, they can team up to give you solid protection in various situations. Here's a quick rundown of their key similarities and differences:

Do you really need both life insurance and health insurance?

Short answer: yeah, probably. But here's the lowdown: having both in your corner—plus some extra cover like critical illness, income protection, and TPD insurance—can give you and your crew an added layer of financial safety net.

Take, for example, the scenario where you're hit with a cancer diagnosis. It's a tough blow, no doubt. But with health insurance, you might have coverage for things like hospital stays or chemo sessions, depending on your plan.

Now, with critical illness insurance, you can get a lump sum payment to help tackle those big-ticket items, like extra treatment costs, travel expenses for hospital visits, or even a well-deserved vacay once you're back on your feet. Because hey, you deserve a break after all that, right?

When life throws you a curveball like a cancer diagnosis, you'll want all the backup you can get. That's where having a mix of insurance types comes in handy.

Why hang on to life insurance when you’ve got health cover?

Relying solely on health insurance might leave some gaps in your financial safety net. While it's great for covering medical bills and treatments, it won't step in to replace lost income or dish out a lump sum if you're dealing with a critical illness or injury. That's where life insurance comes in clutch—it swoops in to fill those gaps, offering extra layers of protection for you.

Finding your life insurance match

Choosing the right life insurance option is a personal decision, tailored to your unique circumstances. Consider factors such as your current income, debt level, and dependents—who relies on your income for expenses like mortgages or education fees? What would happen to your family if you were unable to work due to illness or injury?

When evaluating insurance options, look into aspects like waiting periods, cover inclusions and exclusions, as well as the policy's terms and conditions. Have a chat with your financial adviser to choose a policy that aligns with your needs and financial situation.

Additionally, assess your household budget to ensure you can comfortably afford the insurance premiums associated with the policy.

Having both health and life insurance offers comprehensive coverage for various scenarios. With life insurance, it's essential to explore different options tailored to your individual needs.