Can you get life insurance with a mental health condition?

Here's a topic that’s often misunderstood: life insurance with mental health conditions. There are a few myths out there that can make the whole thing seem more complicated than it really is. Understanding what you can be covered for is key to choosing the best options for your situation.

A lot of people think that if they’ve ever had a mental health condition, they’re automatically out of the running for life insurance. But the truth is, it’s not that black and white. Whether or not you can get covered depends on a range of factors, and more often than not, you can find a life insurance policy that suits your needs. Let's dive into the details and clear up some of these common misconceptions.

Source: Zurich Underwriting Information Factsheet - Mental Health

Understanding mental health claims on your policy

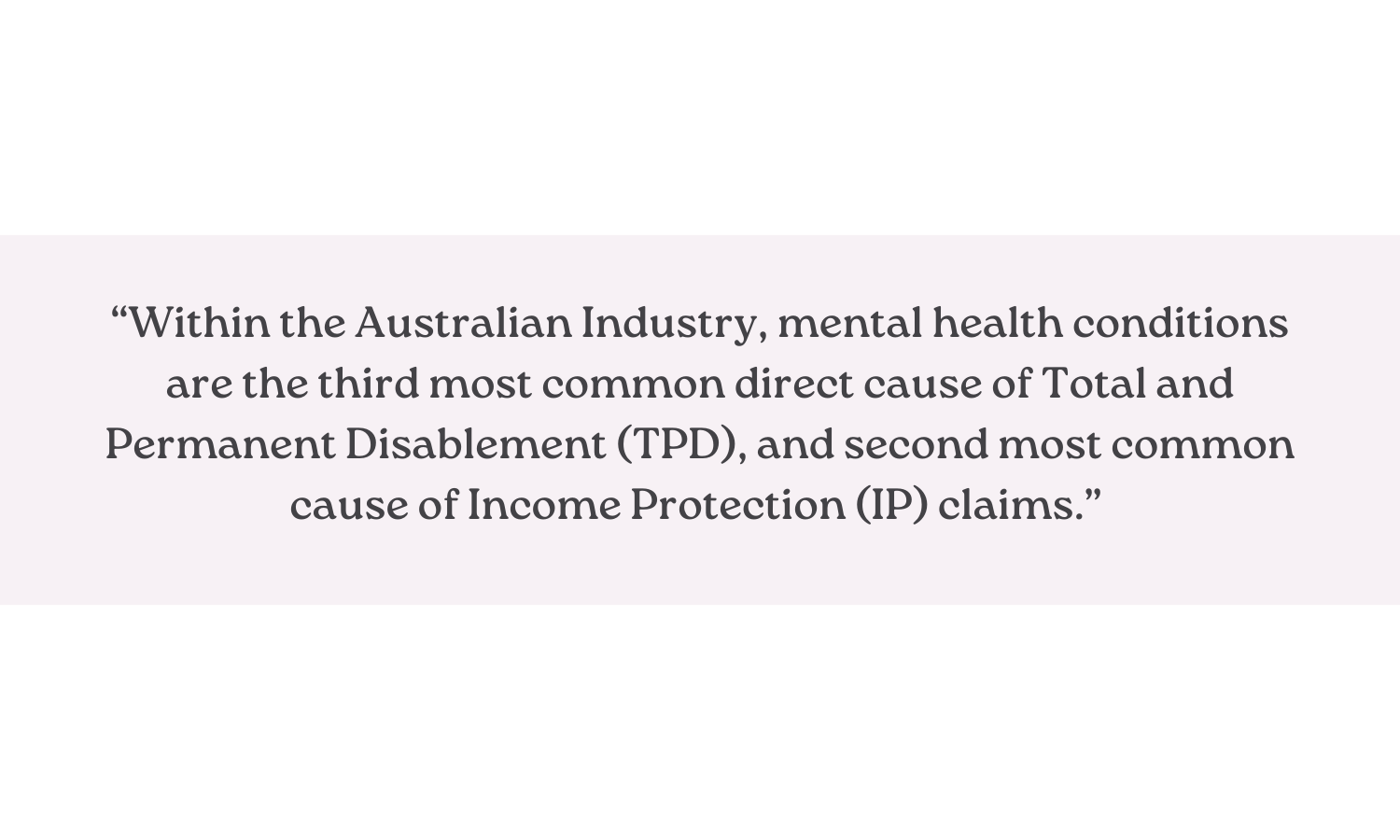

Whether you can make a claim for mental health depends on your specific situation. It's crucial to chat with your financial adviser about your options and make sure you thoroughly understand your Product Disclosure Statement (PDS) and policy schedule. The PDS will outline exactly what is and isn’t covered under your policy, while the policy schedule will indicate any additional exclusions that might apply.

To give you some peace of mind, many people successfully make claims for mental health each year. So, if you’re dealing with a mental health condition, it doesn’t automatically mean you’re out of luck when it comes to life insurance. Just make sure you get all the details and advice you need to make an informed decision.

Source: Zurich Underwriting Information Factsheet - Mental Health

What do underwriters look at?

Underwriters are the folks hired by life insurers to assess the risk of your insurance application. They help decide how much life insurance cover you can get and at what cost.

Here’s what they typically consider when evaluating your application:

Previous diagnoses: Any mental health conditions you’ve been diagnosed with in the past.

Impact on work or study: How your symptoms have affected your ability to work or study.

Severity and management: The severity, duration, and nature of your symptoms, and how you’re managing them.

Lifestyle and overall health: Your lifestyle, general health, work environment, and family medical history.

Current and past treatments: The types of treatment you’re receiving or have received, like therapy or medications.

For instance, if you've been seeing a therapist for anxiety and managing it well with regular sessions and medication, the underwriters will take that into account. They’ll look at how stable your condition is and how it impacts your daily life. This thorough evaluation helps them make a fair decision about your cover.

To know more about how the underwriting process works, head over to this article. Understanding the process can give you better insight into what to expect and how to prepare your application effectively.

How do pre-existing conditions affect your policy?

Mental health conditions can change over time, and they can sometimes lead to new or recurring symptoms. While one mental health condition doesn’t necessarily cause another, having one condition might increase the risk of developing another. For example, if you've had depression, you might be more likely to experience anxiety disorders.

Insurers evaluate each customer based on their unique circumstances. Sometimes, they may add extra charges (called loadings) or exclusions to a policy. However, if the condition presents minimal risk, they might cover you without any additional costs or exclusions.

For instance, if you've managed your mental health condition well over the past few years and it hasn't affected your work or daily life, the insurer might consider you a lower risk. On the other hand, if you’ve had frequent episodes or hospitalisations, there might be loadings or exclusions added to your policy.

If you have a mental health condition and are considering life insurance, it's a good idea to chat with your financial adviser. They can help you navigate the process and find a policy that suits your personal situation.